Union Pacific and Norfolk Southern executives touted their proposed merger as a way to return to volume growth after losing market share to trucks since rail traffic peaked in 2006.

“We can only go so far independently. And let’s face it, this industry has faced contraction over the last couple decades in terms of volume growth,” NS Chief Executive Mark George told investors and analysts on a conference call this morning. “We’ve been losing share to truck — and this is one way to reverse that trend.”

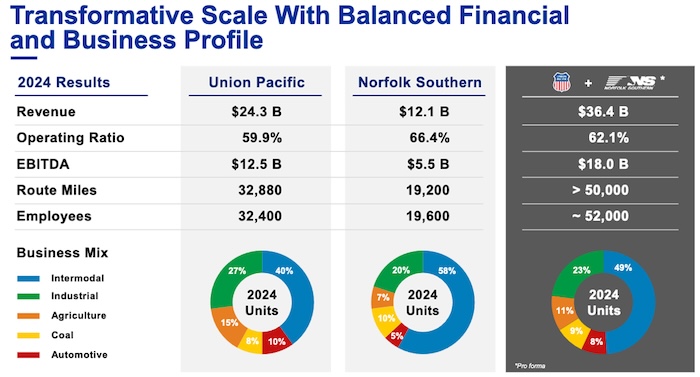

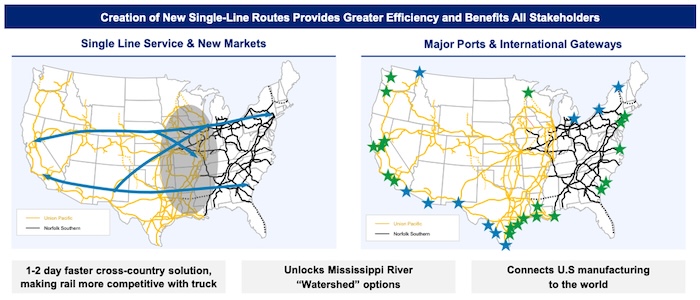

The historic combination — which would create the first transcontinental railroad in the U.S. — would unleash growth by eliminating problematic interchanges, speeding and simplifying service, and enabling the railroad to tap the so-called watershed markets along the Mississippi River. UP and NS envision reeling in $1.75 billion in growth-related revenue by the third year of their merger.

UP (NYSE: UNP) and NS (NYSE: NSC) currently exchange about 1 million shipments per year and are each other’s largest interchange partners. Single-line service will reduce strain on gateways such as Chicago and Memphis, end inefficient crosstown rubber-tire intermodal interchanges, and allow customers to receive rate quotes and bills from one railroad rather than two.

“In the future, those million carloads will immediately see a 24- to 48-hour improvement in their transit time,” Vena said. “That combination of faster service and greater market reach is powerful, making our transcontinental railroad an attractive choice for both current and future customers.”

The transcontinental system’s traffic opportunities include providing seamless service from coast to coast — and most places in between — for intermodal, finished vehicles, food and beverage, chemicals, and steel shipments.

For intermodal and carload, the merger would open up service in the nation’s midsection that’s currently not well-served by rail due to the short hauls for the eastern or western carrier, or both.

“With our interchange with UP today, 95% of our interchange is over 2,000 miles, meaning only 5% is under 2,000 miles. We see an enormous opportunity to grow in lanes where we would be in that 1,000-mile or 1,500-mile range,” George said of intermodal. “So that’s just one example, and that kind of touches upon the entire watershed story.”

Railroads are not competitive on short-haul moves in the watershed, an underserved area that stretches from Wisconsin and Minnesota to eastern Texas, Louisiana, and Mississippi.

“When you’re going from west of it to east, or east to west, rail is never even contemplated because it’s just too much hassle, too much extended time, and frankly, too much cost,” George said. “So these are the areas where we see tremendous growth.”

Single-line service through the watershed on a combined UP-NS system would enable the railroad to compete for traffic moving between Houston and Charlotte, N.C., and Dallas and Columbus, Ohio, for example.

“There’s an awful lot of opportunity here where there’s virtually no rail moves. It’s all truck moves, and those are big markets,” George said, adding that revenue growth from truck conversion likely would exceed the railroads’ $1.75 billion estimate.

A merger also would allow the railroads to eliminate intermediate handlings for carloads.

“We will remove touch points, and every time there’s a touch point, you add 24 to 36 hours, even at the best, while you’re switching the rail car. That’s gone,” Vena said. “On top of that, at the interchange points, where we used to stop and hand off, those are removed. So every customer that today, when we are finally approved … we’re going to cut a day or two off of every transit time.”

And that, he says, will reduce costs for customers, who can reduce the size of their car fleets due to faster cycle times. It also will mean a more fluid railroad.

For new through trains, Chicago will become just another crew change point on the map. But Vena says it’s unlikely that there will be massive swings of volume away from Chicago, a chronic chokepoint where 25% of rail traffic originates, terminates, or passes through.

“We don’t see a huge amount of business changing from Chicago to go to Memphis or go to New Orleans because the out of route miles just don’t add up,” Vena said.

The transcontinental UP also will be able to repatriate international intermodal traffic that Canadian ports, particularly at Vancouver and Prince Rupert, British Columbia, have lured away from U.S. ports over the past two decades, Vena said.

The approval process

Executives also expressed confidence that their deal could gain regulatory approval. The UP-NS combination will be the first judged under the Surface Transportation Board’s 2001 merger review rules. The rules require a merger of Class I railroads to enhance competition — not merely preserve it — and to be in the public interest.

Vena said that if the STB systematically reviews the deal while asking if a transcontinental railroad is better for customers and the country, they will approve it. “We’re very confident of that, or we wouldn’t have taken the step,” he said.

Only 20 customers are currently jointly served by UP and NS where their networks overlap in the Midwest. “We intend to provide a competitive alternative,” Vena said, noting that specifics will be included in the merger application.

The railroads also structured their deal without the use of a voting trust. Rail mergers have typically involved placing the railroad being acquired into a voting trust in order to maintain the railroad’s independence and to allow its stockholders to cash out while the merger is under regulatory review.

The STB in 2021 rejected Canadian National’s (NYSE: CNI) request to put Kansas City Southern in a voting trust, saying it wasn’t in the public interest. The decision scuttled the proposed CN-KCS merger and led to the Canadian Pacific (NYSE: CP)-KCS combination, which was judged under the less restrictive old merger review rules due to an exemption granted to KCS, by far the smallest of the Class I railroads.

UP and NS are not taking that chance.

“We actually believe that a voting trust would complicate and potentially delay the transaction,” UP Chief Financial Officer Jennifer Hamann said. “So we want to go to the STB with a fully developed merger application that allows us to really lay out the fundamentals of this merger and provide all the necessary details that supports our position that this will not only enhance competition, but is absolutely in the public interest.”

Plus, without a voting trust UP won’t have to fund the deal until it gains STB approval, which is estimated for 2027 based on the STB’s statutory guidelines.

Promises of smooth integration

Railroad mergers in the modern era have had one thing in common: Service problems that occur while meshing operations and information technology systems.

UP’s operational decisions in Houston after the 1996 acquisition of Southern Pacific created a massive traffic jam in 1997 and 1998. On the heels of that, information technology problems led to immediate service problems on Norfolk Southern after the 1999 split of Conrail with CSX (NASDAQ: CSX), which later stumbled with its own service issues.

“A transaction of this size and scope won’t be easy to execute. We understand that,” Vena said.

The railroad will maintain adequate reserves of locomotives, train crews, and other resources in order to be able to better respond and recover to service issues, he said.

“We’re very aware of what led to the merger moratorium back in the 2000, 2001 time frame, and it was just a bunch of bad integrations,” George said. “And we are committed to make sure that doesn’t happen in this case.”

The two-year review process will allow sufficient time for planning, George said, particularly on information technology systems.

CPKC’s problematic computer cutover this past May in former KCS territory in the U.S. produced congestion, missed switches, and delays that CPKC has now mostly mopped up.

Last year UP had a smooth cutover to its new cloud-based NetControl computer system, which processes everything from rail car inventory and scheduling to waybill processing and train, locomotive, and terminal management. “It was a non-event,” Vena said. “It was like nobody knew it actually happened.”

Much of the $2 billion the railroads have earmarked for increased capital spending will go toward information technology investments.

Merger synergies of $2.75 billion

Assuming shareholders approve the deal, UP will acquire NS in a stock and cash transaction that values NS at $320 per share, a 25% premium. The combined company would have an enterprise value of more than $250 billion. The railroads said the merger would create $2.75 billion in annual synergies, split between $1.75 billion in revenue growth and $1 billion in cost and productivity savings.

UP will finance $20 billion of the deal through a combination of cash on hand and new debt. Both railroads will stop their share buyback programs through 2028 but will maintain dividend payments.

Shipper and labor opposition

The railroads pledged to preserve union jobs, which are the vast majority of the combined system’s 52,000-strong workforce.

“All of our union employees who have a job today will have jobs tomorrow in our merged company,” Vena said. “And a company that is growing its business and spurring economic development creates even more jobs.”

Nonetheless, the SMART-TD union that represents conductors said it would oppose the merger.

Yesterday shipper associations told Trains that they would oppose further consolidation in the rail industry.

How will the railroads handle objections from shippers and rail labor?

“We’ll handle them one by one, but I think as people start to come to understand what we’re putting forward, they’re going to see the benefits,” George said.

That especially applies to labor because the company would add jobs as it gains new traffic, he said.

Subscribe to FreightWaves’ Rail e-newsletter and get the latest insights on rail freight right in your inbox.

Related coverage:

Shippers line up against railroad mergers

Union Pacific and Norfolk Southern reach $85 billion merger deal

First look: Norfolk Southern earnings

Bill aims to prioritize rail freight, untangle congestion

The post CEOs say Union Pacific-Norfolk Southern merger will reverse rail freight decline appeared first on FreightWaves.